In this article

- 1. Why Do Businesses Even Need A Trial Balance?

- 2. What Exactly Is A Trial Balance?

- 3. What Does A Trial Balance Actually Look Like?

- 4. Are There Different Types of Trial Balance?

- 5. Can A Trial Balance Detect Every Accounting Error?

- 6. Where Do Many Business Owners Get Confused?

- 7. Does Accounting Software Make Trial Balances Obsolete?

- 8. Final Thoughts

- 9. Trail Balance FAQs

A lot of business owners only hear the term trial balance when their accountant brings it up at year-end.

Usually, it happens during a discussion about financial statements, tax submissions, or audit preparation. Someone mentions that the trial balance is ready, everyone nods, and the conversation moves on.

The funny thing is that this report, despite rarely being discussed outside accounting circles, sits right at the centre of accurate financial reporting.

Without it, preparing reliable accounts would be far more difficult.

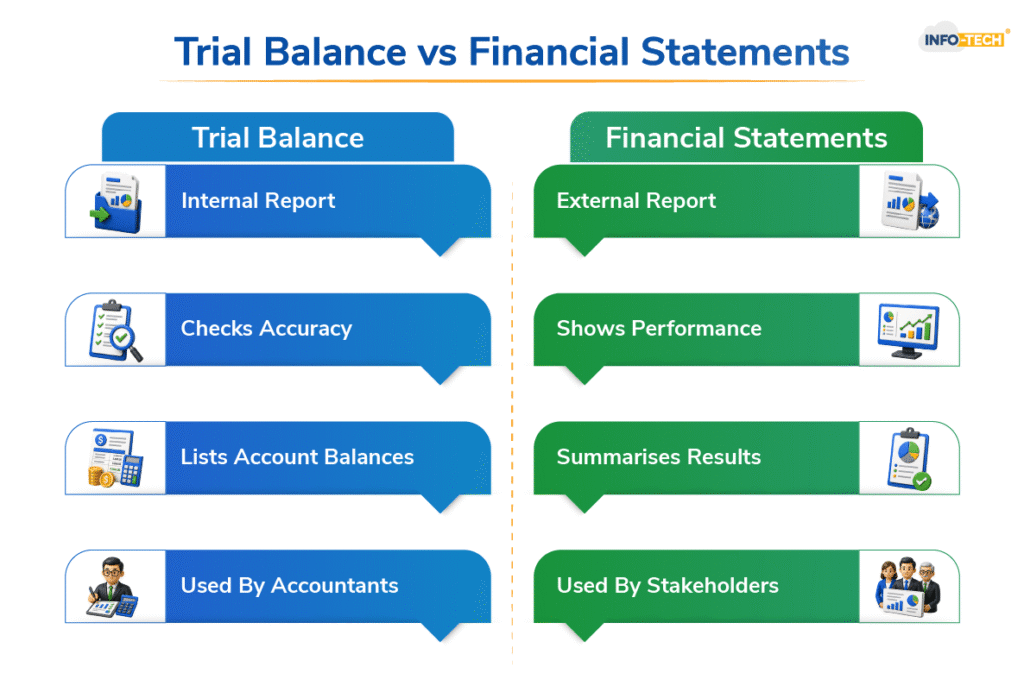

Most people are familiar with reports like the balance sheet or profit and loss statement because those documents tell a story about how a business is performing. A trial balance is different. It doesn’t tell you whether you’re making money, doesn’t show how much cash you have in the bank, nor does it tell you whether sales are increasing or falling.

Instead, it performs a much simpler job.

It checks whether the accounting records behind those reports are balanced.

That might sound like a small detail, but for accountants, it’s one of the first things they want to know before trusting any set of financial numbers.

Why Do Businesses Even Need A Trial Balance?

Imagine running a small business for a year.

Customers place orders. Suppliers send invoices. Rent gets paid every month. Staff salaries are processed. Utility bills arrive. New equipment is purchased. Loan repayments leave the bank account.

Now imagine keeping track of every one of those transactions.

By the end of the year, even a relatively small company could have hundreds of accounting entries sitting inside its records. Larger businesses may have thousands.

With that many transactions flowing through the books, mistakes become inevitable.

A payment might be recorded twice.

An invoice could be entered incorrectly.

A figure may be posted to the wrong account.

This is where the trial balance earns its place.

Rather than checking transactions one by one, accountants use the trial balance to review all account balances together and confirm that the books are still mathematically balanced.

It’s a bit like checking the foundations of a building before adding another floor. If something is wrong at the base level, it makes little sense to continue building on top of it.

So, What Exactly Is A Trial Balance?

In simple terms, a trial balance is a report that lists every account in a company’s ledger together with its balance at a particular date.

These balances are divided into two columns:

- Debits

- Credits

Because accounting follows a double-entry system, the total value of debits should always equal the total value of credits.

When they don’t match, it’s usually a sign that something has gone wrong somewhere in the accounting records.

When they do match, it suggests that the books are balanced from a mathematical perspective.

That doesn’t automatically mean everything is perfect, but it does provide a level of reassurance before financial statements are prepared.

Think about it this way.

Before an accountant starts preparing reports that business owners, banks, auditors, or tax authorities may rely on, they want to know that the numbers are internally consistent.

The trial balance helps answer that question.

What Does A Trial Balance Actually Look Like?

Despite its importance, a trial balance is surprisingly straightforward.

It is essentially a list of account balances pulled from the general ledger.

A simplified version might look something like this:

| Account | Debit (RM) | Credit (RM) |

| Cash | 50,000 | |

| Inventory | 20,000 | |

| Equipment | 30,000 | |

| Accounts Receivable | 15,000 | |

| Accounts Payable | 12,000 | |

| Bank Loan | 40,000 | |

| Sales Revenue | 63,000 | |

| Total | 115,000 | 115,000 |

The important part isn’t the individual figures.

It’s the total at the bottom.

If both sides agree, the accounting records are balanced.

If they don’t, accountants know they have some investigating to do.

Are There Different Types of Trial Balance?

Although people often talk about the trial balance, accountants usually work with three different versions during the accounting cycle.

Unadjusted Trial Balance

This is the first trial balance prepared after everyday transactions have been recorded. It shows the account balances before any year-end adjustments are made.

Adjusted Trial Balance

Once adjustments such as depreciation, accrued expenses, or prepaid expenses have been recorded, an adjusted trial balance is prepared. This is the version used to produce the financial statements.

Post-Closing Trial Balance

After revenue and expense accounts have been closed for the year, a post-closing trial balance is prepared. It contains only permanent accounts that carry forward into the next accounting period.

Can A Trial Balance Detect Every Accounting Error?

Not quite.

A trial balance can confirm that total debits and credits are equal, but that doesn’t mean every transaction has been recorded correctly. Some mistakes won’t affect the balance at all.

Common examples include:

- Error of Omission – A transaction is left out completely.

- Error of Commission – A transaction is posted to the wrong account of the same type.

- Error of Principle – A transaction is recorded under the wrong account category, such as treating equipment as an expense.

- Compensating Errors – Two separate mistakes cancel each other out.

- Reversal Errors – The debit and credit entries are accidentally swapped.

This is why accountants don’t rely on the trial balance alone. They also review supporting documents, reconcile accounts, and investigate anything that looks unusual before finalising the financial statements.

Where Do Many Business Owners Get Confused?

A common assumption is that a balanced trial balance means everything is correct.

Unfortunately, accounting isn’t always that straightforward.

A trial balance can tell you that debits and credits match. It cannot tell you whether every transaction has been recorded in the right place.

For example, imagine a company purchases a vehicle but accidentally records it as office equipment.

The books may still balance.

Or perhaps an invoice gets entered twice.

The books may still balance.

Even missing transactions can sometimes escape detection if both sides of the entry were omitted entirely.

This is why accountants don’t stop at the trial balance. They use it as a starting point, not a final answer.

It’s one piece of the puzzle, alongside reconciliations, reviews, supporting documents, and financial analysis.

Also Read: What Is Bookkeeping In Malaysian Business?

Does Accounting Software Make Trial Balances Obsolete?

Not really.

Modern accounting software has made preparing a trial balance much faster than it was twenty years ago.

Instead of manually compiling account balances, most systems can generate a report within seconds.

But software doesn’t eliminate the need for review.

If someone records a transaction incorrectly, the software will process that mistake just as efficiently as it processes a correct entry.

That’s why accountants still review trial balances today, even in businesses that have fully embraced digital accounting systems.

Technology has changed the speed of accounting.

It hasn’t changed the need to verify the numbers.

Final Thoughts

The trial balance isn’t the most glamorous report in accounting, and most business owners will never need to study one in detail.

Even so, it plays a crucial role behind the scenes.

Before financial statements are produced, before audits begin, and before tax figures are finalised, accountants often turn to the trial balance to make sure the books are standing on solid ground.

For Malaysian businesses, it’s one of those reports that quietly supports accurate financial reporting without attracting much attention.

Solutions such as Info-Tech Accounting Software help businesses keep financial records organised, generate real-time accounting reports, and produce trial balances instantly. By reducing manual data entry and providing a clearer view of financial information, businesses can spend less time checking numbers and more time focusing on growth.