In this article

- 1. What Is the Private Retirement Scheme (PRS)??

- 2. Why Was PRS Introduced When Malaysians Already Have EPF?

- 3. What Is Private Retirement Scheme Tax Relief?

- 4. Who Can Claim Private Retirement Scheme Tax Relief?

- 5. How Much Private Retirement Scheme Tax Relief Can You Claim?

- 6. Conclusion

- 7. PRS Tax Relief – Private Pension Administrator Malaysia (PPA) FAQs

If you ask most Malaysians what they’re saving for, retirement probably won’t be the first answer you hear.

A home is usually higher on the list. Paying off a car loan, building an emergency fund, or setting aside money for children’s education tends to feel far more immediate. Retirement sits somewhere in the distance, quietly waiting for a future version of ourselves to deal with.

That’s hardly surprising.

When retirement is twenty or thirty years away, it’s difficult to picture what life will actually look like. There’s always the assumption that there will be more time to save later. Before you know it, a decade has passed, and that “later” suddenly doesn’t feel so far away.

This is exactly why the Malaysian Government encourages long-term retirement planning instead of relying solely on compulsory savings. While the Employees Provident Fund (EPF) remains the backbone of retirement income for many workers, it was never intended to be the only source of financial security after retirement.

The Private Retirement Scheme (PRS) was introduced to give Malaysians another option. More importantly, contributors may also enjoy private retirement scheme tax relief, making it one of the few financial decisions that can benefit both your future and your current tax position at the same time.

If you’ve heard friends or colleagues mention PRS during tax season but never really understood what it is, you’re certainly not alone. Many people know there’s a tax benefit attached to it, yet they’re unsure how the scheme works, who manages it, or whether it’s actually worth contributing to.

The good news is that it’s much simpler than it first appears.

What Is the Private Retirement Scheme (PRS)?

Think of PRS as a retirement savings plan that you choose for yourself.

Unlike EPF, nobody is required to contribute. There isn’t an employer deciding how much goes into your account each month, nor is there a legal obligation to participate. Whether you contribute RM100 every month or make occasional lump-sum investments is entirely your decision.

That flexibility is one of the reasons the scheme appeals to so many people.

Some contributors are young professionals who want to start building long-term wealth early. Others are business owners who don’t receive regular EPF contributions in the same way employees do. There are also individuals approaching retirement who simply feel they need another source of savings to complement what they’ve already accumulated.

Rather than sitting in an ordinary savings account, the money contributed to PRS is invested through professionally managed funds offered by approved providers. The objective isn’t short-term gains. It’s steady, long-term growth that can support your retirement years.

Like any investment, returns aren’t guaranteed and can rise or fall depending on market conditions. That’s why PRS should always be viewed as a long-term commitment rather than a product designed for quick profits.

Why Was PRS Introduced When Malaysians Already Have EPF?

This is probably one of the most common questions people ask.

After all, every month employees already contribute to EPF, and employers make contributions as well. Doesn’t that already cover retirement?

The answer depends on the lifestyle someone hopes to maintain after leaving the workforce.

Life expectancy has increased over the years, which means many Malaysians will spend twenty years or more in retirement. Medical expenses are rising, everyday living costs continue to change, and many people understandably want to enjoy retirement rather than simply get by.

EPF remains an essential part of retirement planning, but it was never designed to meet every individual’s future financial needs.

PRS fills that gap by giving people another way to build retirement savings on their own terms. Instead of replacing EPF, it complements it.

Many financial planners describe it as creating another layer of financial security. If your compulsory savings form the foundation, PRS helps strengthen the structure above it.

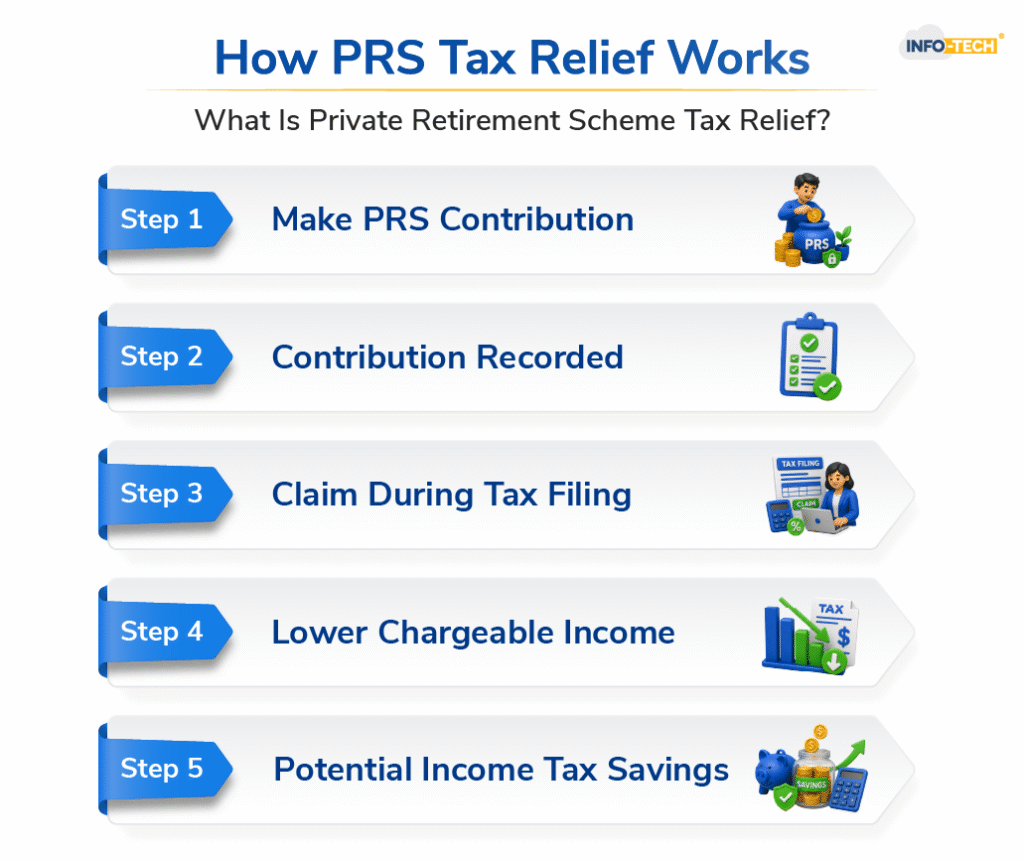

What Is Private Retirement Scheme Tax Relief?

For many contributors, the tax incentive is what first captures their attention.

The private retirement scheme tax relief allows eligible taxpayers to reduce their chargeable income by claiming qualifying PRS contributions when filing their annual income tax return.

This is where some confusion often arises.

People sometimes assume tax relief means getting the same amount back from the Government. That’s not how it works.

Instead, tax relief reduces the amount of income on which your taxes are calculated. If your taxable income becomes lower, the amount of tax you eventually pay may also decrease.

Although the immediate tax savings are attractive, they shouldn’t be the only reason someone contributes to PRS.

The bigger picture is that you’re gradually building a retirement fund while enjoying a tax benefit along the way. One advantage supports the future, while the other provides value today.

Who Can Claim Private Retirement Scheme Tax Relief?

One of the misconceptions surrounding PRS is that it’s mainly for employees working in large companies.

In reality, the scheme is far more accessible than many people realise.

Employees can contribute. So can self-employed individuals, freelancers, professionals and business owners. As long as you make qualifying contributions to an approved PRS fund and meet the requirements set by the Inland Revenue Board of Malaysia (LHDN), you may be eligible to claim the available relief.

Of course, good record keeping is still important.

Most PRS providers issue annual contribution statements, making it easier to support your claim during tax filing. Holding onto these documents is a simple habit that can save unnecessary complications later.

Because tax policies are reviewed from time to time, it’s also sensible to check the latest guidance issued by LHDN before submitting your return instead of relying on figures you’ve seen online from previous years.

How Much Private Retirement Scheme Tax Relief Can You Claim?

Almost everyone asks this question eventually.

The honest answer is that the relief depends on the limit announced by the Government for the relevant Year of Assessment.

Tax incentives are occasionally revised as part of Malaysia’s annual Budget, so the maximum amount available today may not necessarily remain the same in future years.

That’s why financial advisers usually recommend checking the latest information published by LHDN before filing your taxes. It only takes a few minutes, but it helps ensure you’re claiming the correct amount under the current rules.

What’s more important than chasing the maximum deduction is developing the habit of contributing consistently. Retirement planning is rarely about making one large contribution. More often, it’s the result of small decisions repeated over many years.

Conclusion

For many Malaysians, retirement still feels like something that can wait. There’s always another financial priority that seems more urgent, whether it’s paying off a home loan, supporting your family, or building your career. But the truth is, retirement planning doesn’t become easier by putting it off. If anything, the earlier you start, the more time your savings have to grow.

That’s where the Private Retirement Scheme can make a real difference. It isn’t meant to replace EPF or guarantee a comfortable retirement on its own. Rather, it’s another tool that allows you to strengthen your long-term financial plans while making use of the private retirement scheme tax relief available under current tax rules.

If you’re looking for a simpler way to manage your finances, an Accounting Software helps businesses maintain accurate financial records, generate reports, and stay on top of their accounting responsibilities.

Whether PRS is the right choice depends on your own financial circumstances, but understanding how it works is a sensible first step. A little planning today may not seem like much, but years down the road, you’ll probably be glad you started when you did.