In this article

- 1. Why EPF Is Important?

- 2. A Bit of Background About EPF

- 3. Who Needs to Contribute to EPF?

- 4. How EPF Contributions Work?

- 5. Where Does Your EPF Money Go?

- 6. How Employers Submit EPF?

- 7. How To Register for EPF?

- 8. What Happens If Employers Don’t Follow the EPF Rules?

- 9. Closing Thoughts

- 10. Employees Provident Fund FAQs

If you’ve worked in Malaysia, you’ve definitely heard of EPF. It’s one of those things that shows up on your payslip every month, but not everyone fully understands how it works.

The Employees Provident Fund (EPF) has been in use since 1951. It started as a basic savings plan for workers who didn’t have pensions, and today, it’s grown into one of the biggest retirement funds in the region. Millions of Malaysians rely on it as their main form of retirement savings.

Whether you’re an employer handling payroll or an employee trying to make sense of your deductions, knowing how EPF works really makes a difference in the long run.

Why EPF Is Important?

Most people look at EPF as just another deduction from their salary. But in reality, it’s building up your future savings slowly, month by month.

Right now, EPF supports more than 14 million members. That alone shows how important it is to the country’s workforce. What makes EPF useful is that:

- You’re not saving alone; your employer contributes too

- It forces consistent saving

- The money is invested, so it grows over time

For many Malaysians, this ends up being their biggest financial backup after retirement.

A Bit of Background About EPF

EPF didn’t always look like what it is today. It began during the colonial period and later evolved after Malaysia became independent.

Now, it’s managed under the Ministry of Finance and operates based on the EPF Act 1991. There are different groups managing different parts like investments, risk, and Shariah compliance to make sure everything runs properly.

You don’t really need to remember all the terms, but it helps to know that the system is structured and monitored closely.

Who Needs to Contribute to EPF?

In most cases, EPF is not optional.

If you’re:

- A Malaysian working in the private sector

- A permanent resident employed locally

- All non-Malaysian citizen employees holding valid employment passes (excluding domestic workers)

then you’re automatically part of it.

Note: Starting 1 October 2025, EPF contributions became mandatory for all non-Malaysian citizen employees holding valid employment passes (excluding domestic workers), with both employer and employee each required to contribute 2% of monthly wages.

Some government contract workers also contribute.

If you’re self-employed, you won’t be forced to contribute, but you can still do it voluntarily if you want to save for retirement.

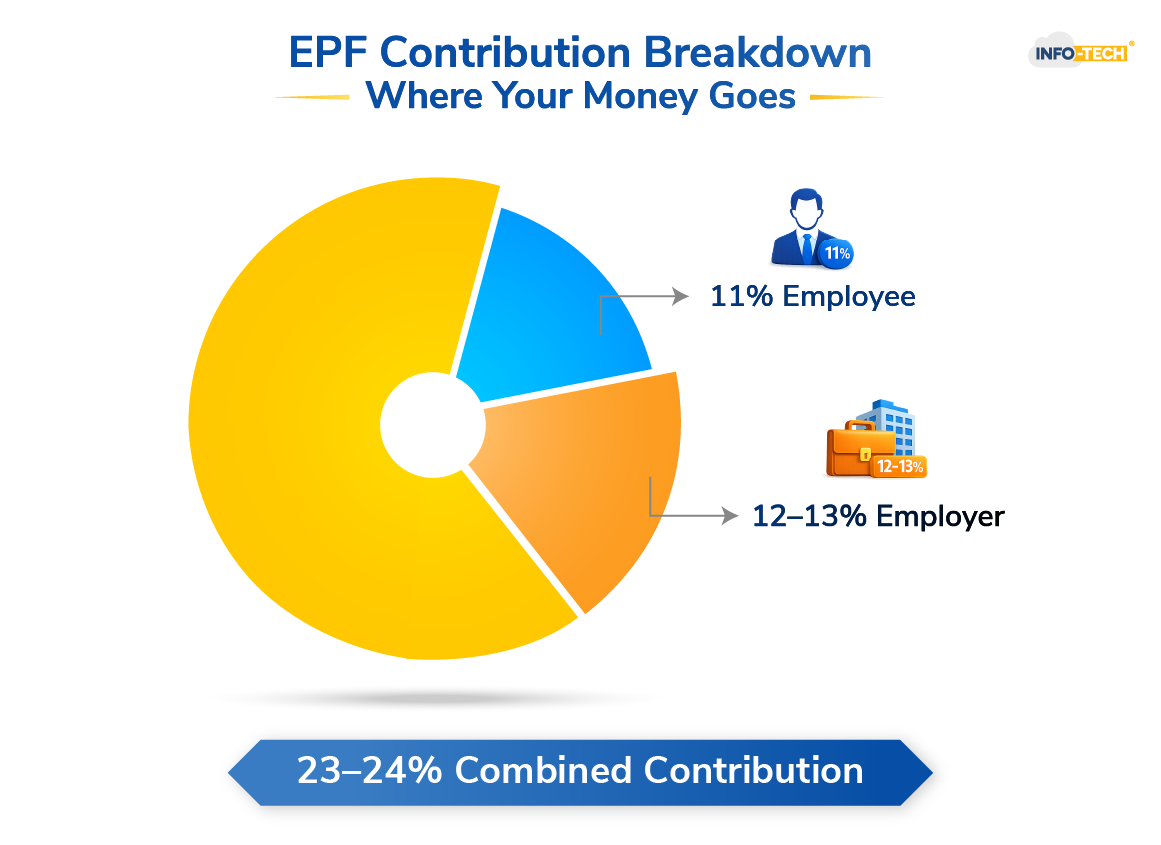

How EPF Contributions Work?

Every month, a portion of your salary goes into EPF and your employer adds their share on top of that.

Here’s a simple breakdown:

| Category | Employee Contribution | Employer Contribution | Total |

| Below 60 (≤ RM5,000 salary) | 11% | 13% | 24% |

| Below 60 (> RM5,000 salary) | 11% | 12% | 23% |

| 60 and above (Malaysians) | 0% | 4% | 4% |

These rates aren’t always fixed forever; sometimes the government adjusts them depending on the economy.

Employers need to submit these contributions by the 15th of every month. Missing that deadline can cause issues.

Where Does Your EPF Money Go?

Your savings are actually split into different accounts.

- Account 1 (70%) This is mainly for retirement. You usually can’t touch it until you turn 55.

- Account 2 (30%) This one is more flexible. You can use it for things like:

- Buying a house

- Paying for education

- Medical expenses

There are also newer options like Shariah savings if you prefer investments that follow Islamic principles.

How Employers Submit EPF?

Most companies don’t do this manually anymore. There are a few common ways:

It’s mostly digital now, which makes things faster and easier to track.

How To Register for EPF?

Most of the time, you don’t even need to do anything. You’re usually registered automatically when your employer makes your first contribution.

If not, you can:

- Go to an EPF counter with your MyKad

- Use a Smart Kiosk

- Let your employer handle it through their system

Once it’s done, you’ll get your EPF member number.

What Happens If Employers Don’t Follow the EPF Rules?

EPF compliance is taken very seriously in Malaysia.

If an employer:

- Doesn’t register

- Fails to contribute

- Pays late

- Deducts money but doesn’t submit it

they can face fines, penalties, or even legal action.

There are also extra charges added on unpaid contributions, so it can get expensive quickly. That’s why most companies try to stay on top of it.

Closing Thoughts

EPF might not feel exciting, but it’s one of those things that quietly builds your financial security over time.

For employers, it’s something you simply can’t ignore. For employees, it’s worth understanding because it directly affects your future savings.

The more you know about it, the better decisions you can make; whether it’s planning for retirement, buying a house, or just keeping track of your finances.

A cloud payroll software can take a lot of stress out of handling EPF, mainly for employers who deal with it every month. Instead of calculating contributions manually, the system does it automatically based on the latest EPF rates. This ensures that both employee and employer contributions are calculated correctly every time.

Info-Tech helps you eliminate human errors in payroll calculations. Get in touch today!

Employees Provident Fund FAQs

How can I check my PF balance?

You can check your EPF balance in Malaysia by logging into i-Akaun (KWSP) online or through the KWSP mobile app. Alternatively, visit an EPF kiosk or branch and use your MyKad for instant access.

Can I withdraw 100% of my EPF?

Yes, you can withdraw 100% of your EPF savings when you reach age 55 (or 60, depending on your choice), or if you permanently leave Malaysia or pass away (for nominees/beneficiaries). Otherwise, only partial withdrawals are allowed for things like housing, education, or medical needs.

Can I still contribute to EPF after 60 years of age?

Yes, you can still contribute to EPF after age of 60. However, it’s optional at that stage, and the contribution rate is lower. Typically, only the employer contributes (around 4%), while employees are no longer required to contribute unless they choose to do so voluntarily.

Can I withdraw EPF dividends after 60?

Yes, after the age of 60, your EPF savings (including dividends earned each year) remain in your account, and you can withdraw them anytime, either fully or partially. The dividends are already included in your total balance, so when you withdraw, you’re withdrawing both your savings and the dividends together.