For most people in Malaysia, EPF is something that quietly runs in the background. You see the deduction on your payslip every month, your employer contributes their share, and over time, the balance grows. But it usually stays out of sight—until the moment you actually need the money.

That’s when the questions start.

“Can I withdraw this?”

“How much can I take?”

“Will it affect my future?”

EPF isn’t just a savings pool you can dip into anytime. It’s structured with a purpose—to protect your retirement while still giving you access when life truly demands it. Understanding how that balance works is what makes all the difference.

What EPF Is Really Designed For

At its core, EPF is a long-term financial safety system. It ensures that when your working years slow down or stop completely, you’re not left without income. Here’s what happens every month:

- A portion of your salary is contributed

- Your employer adds their contribution

- EPF invests these funds and generates dividends

Over time, this builds into a significant amount.

👉 That’s why EPF doesn’t allow unrestricted withdrawals. It’s not about limiting you—it’s about making sure your future is still secure.

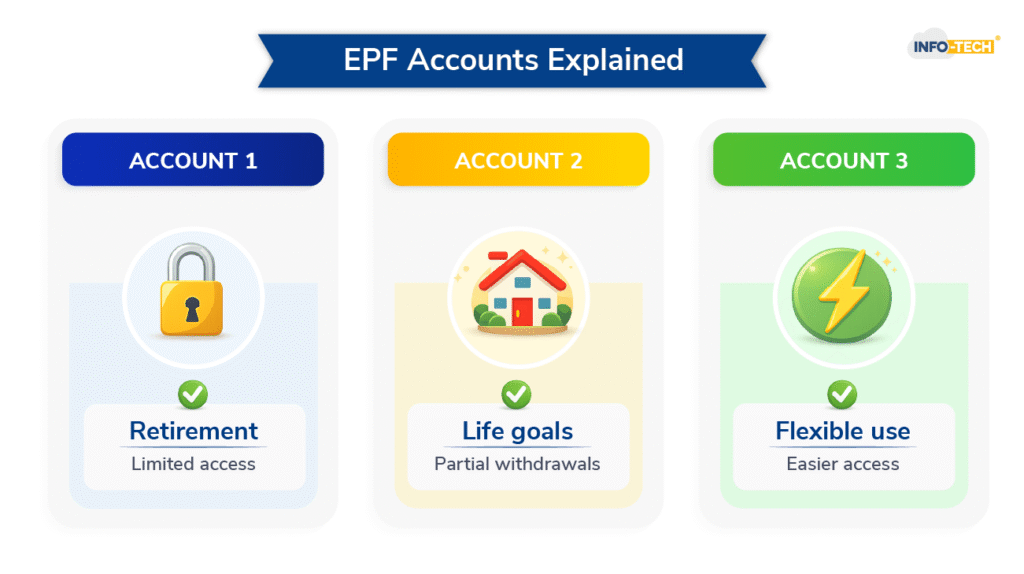

How Your EPF Savings Are Structured

One of the most important things to understand is that your EPF money is not sitting in one single pool. It’s divided into accounts, and each account has a specific role.

| Account | Purpose | Withdrawal Flexibility |

| Account 1 | Retirement savings | Very limited (mainly after 55) |

| Account 2 | Pre-retirement needs | Partial withdrawals allowed |

| Account 3 (Flexible) | Short-term needs | More flexible access |

To put it simply:

- Account 1 is your future survival fund

- Account 2 supports major life milestones

- Account 3 offers controlled flexibility

This structure ensures that even if you withdraw some money today, you don’t completely compromise your retirement.

When You Can Withdraw EPF

EPF withdrawals are not based on convenience—they are based on purpose. You can withdraw your savings, but only when your reason fits into approved categories. There are three main situations where withdrawals are allowed.

1. Pre-Retirement Withdrawals (Before Age 55)

This is where most people interact with EPF withdrawals. You are allowed to withdraw your savings early, but only for meaningful, long-term purposes—not everyday spending. Common Approved Withdrawal Reasons

- Housing

- Buying a home

- Building a house

- Reducing housing loans

- Education

- Tuition fees for approved institutions

- Local and overseas studies

- Medical Needs

- Critical illness treatment

- Medical equipment and procedures

- Hajj

- Pilgrimage expenses (subject to conditions)

- Leaving Malaysia

- Permanent migration or renouncing citizenship

Each of these withdrawals typically comes from Account 2, and every application must be supported with proper documentation.

👉 This is EPF’s way of ensuring withdrawals are tied to real, impactful needs.

2. Age-Based Withdrawals

As you move closer to retirement, EPF gradually gives you more control over your savings. Key Age Milestones

| Age | What You Can Do |

| 50 | Partial withdrawal (Account 2) |

| 55 | Full withdrawal allowed |

| 60 | Continued withdrawals + dividends |

At age 55, your EPF savings become fully accessible. But this is also where many people make rushed decisions. Instead of withdrawing everything at once, many choose:

- Monthly withdrawals for steady income

- Partial withdrawals to preserve savings

- Keeping funds in EPF for continued dividends

👉 Retirement today can last 20–30 years, so how you withdraw matters as much as when.

3. Special or Emergency Withdrawals

There are times when EPF introduces special withdrawal schemes, usually during national crises. Examples include:

- COVID-19 withdrawal programs (i-Sinar, i-Citra)

- Economic relief initiatives

These are temporary measures—not part of standard EPF policy—but they show that the system can adapt when necessary.

What You Need Before Applying

This is one of the most overlooked parts of the process. You cannot withdraw EPF based on intention alone—you need proof.

| Withdrawal Type | Required Documents |

| Housing | Sale & Purchase Agreement |

| Education | Offer letter / fee breakdown |

| Medical | Doctor’s report + medical bills |

| Migration | Proof of relocation |

👉 Missing or incorrect documents are one of the biggest reasons for delays or rejections.

How the EPF Withdrawal Process Works

The process today is much simpler than before, thanks to digital access. Step-by-Step Process

- Log in to your i-Akaun (Member Portal)

- Select Withdrawal

- Choose your withdrawal type

- Upload required documents

- Submit your application

- Track status online

Most applications are processed within 3 to 10 working days, depending on verification requirements.

How Much Can You Withdraw

This is where expectations need to be realistic. You usually cannot withdraw everything unless you’ve reached age 55.

| Withdrawal Purpose | Withdrawal Limit |

| Housing | Based on property/loan value |

| Education | Tuition fees only |

| Medical | Actual treatment cost |

| Age 50 | Partial withdrawal |

| Age 55 | Full withdrawal |

👉 EPF limits are designed to protect your long-term financial stability.

Are EPF Withdrawals Taxable?

In Malaysia, EPF withdrawals are generally tax-free, especially when used for approved purposes such as:

- Retirement

- Housing

- Education

- Medical

This makes EPF one of the more efficient financial tools available for long-term planning.

Common Mistakes People Make

Many people only realize their mistakes years later—when their EPF balance is no longer enough. Some of the most common ones include:

- Withdrawing too early without a long-term plan

- Using EPF for non-essential spending

- Not understanding account limitations

- Submitting incomplete applications

👉 The key takeaway: EPF is not extra money—it’s future security.

Smarter Ways to Use EPF

Instead of focusing on access, it helps to focus on impact. A smarter approach to EPF withdrawals includes:

- Using funds for asset-building (like property)

- Avoiding withdrawals for short-term lifestyle expenses

- Taking partial withdrawals instead of full amounts

- Planning withdrawals alongside other financial strategies

This mindset helps you balance present needs without sacrificing future stability.

Why EPF Matters for Employers and HR

For employers, EPF is more than just a statutory requirement—it directly affects employee trust and compliance. Key responsibilities include:

- Ensuring accurate monthly contributions

- Maintaining proper employee records

- Supporting employees with withdrawal documentation

- Staying updated with EPF policy changes

Errors in EPF management can lead to penalties, audits, and employee dissatisfaction.

How Our Software Simplifies EPF Management

Managing EPF manually—especially alongside SOCSO, EIS, and payroll—can quickly become complex. Our HRMS & Payroll Software is designed to simplify this entire process. With our system, you can:

- Automate EPF, SOCSO, and EIS calculations

- Stay compliant with the latest regulations

- Generate accurate payroll and statutory reports

- Reduce manual errors and audit risks

- Maintain organized employee records for easy withdrawal processing

Instead of spending time fixing errors, your team can focus on running the business.

Final Thoughts

EPF withdrawals are not meant to be complicated—but they are meant to be thoughtful. Every withdrawal decision has a long-term impact. While the system allows flexibility, it also encourages discipline. So before making any withdrawal, take a moment and ask:

👉 “Is this helping my future—or taking away from it?” Because at the end of the day, EPF isn’t just about saving money—it’s about securing your life after work.