In Malaysia’s payroll and tax compliance scene, CP8D stands out as a crucial yearly statutory filing that employers must submit to the Inland Revenue Board of Malaysia (LHDN). While it’s often mentioned alongside Form E and EA Form, CP8D has a unique and specific role. This document gives LHDN a complete breakdown of each employee’s annual remuneration enabling the authority to check tax deductions, match up Monthly Tax Deductions (PCB), and ensure income is reported correctly.

As Malaysia keeps strengthening digital tax enforcement through MyTax and e-Data Praisi systems in 2026, CP8D is more than justan administrative requirement. It now serves as a key compliance check that allows LHDN to compare employer payroll data with employee tax filings. Employers who don’t get CP8D submission right or submit late might face fines, raise red flags for audits, and run into relevancy problems.

This guide breaks down CP8D — covering its legal grounds goals how to submit it, what employers need to do, penalties, and common questions.

What Is CP8D?

CP8D is a yearly return from employers that has all the details on remuneration given to employees during a specific tax year.

Companies submit this form to LHDN along with Form E. It has detailed payroll info for each employee, including:

- Employee ID details

- Total yearly gross remuneration

- Allowances and bonuses

- Benefits-in-kind (BIK)

- Director fees (if needed)

- PCB (Monthly Tax Deduction) totals

- EPF payments

Form E gives a summary declaration of what the company paid out. CP8D breaks this down employee by employee, so LHDN can check if everything adds up at an individual level.

To make it simple:

Form E = Employer Summary

CP8D = Detailed Employee Data

EA Form = Income Statement Issued to Employee

How CP8D Fits into Malaysia’s Tax Setup?

CP8D aims to strengthen transparency and make sure income tax deducted through PCB is tracked. The tax system in Malaysia depends a lot on employers’ compliance since PCB works as an advance payment of income tax for employees.

With CP8D, LHDN can:

- Cross-check PCB deductions against actual annual remuneration

- Validate information declared by employees in their e-Filing

- Detect under-reporting or payroll inconsistencies

- Identify discrepancies between EA Forms and employer submissions

- Enhance audit accuracy and compliance monitoring

Without CP8D, LHDN would rely on employer summary data and employee self-declarations, which could create gaps in verification. CP8D fills this gap by bringing in structured payroll reporting.

What Does Rule 8D of the Income Tax Rules Say?

CP8D comes from Rule 8D of the Income Tax (Deduction from Remuneration) Rules 1994.

Rule 8D requires employers to:

- Make a full yearly report of remuneration given to employees

- Hand in the report in the way LHDN prescribed

- Make sure PCB deductions reported are correct

- Turn it in by the set deadline

This rule strengthens the employer’s duty in Malaysia’s self-assessment tax system. Not following it can lead to fines under the Income Tax Act 1967.

At its core, Rule 8D makes CP8D a required report by law, not just a form you can choose to fill out.

What Is The Difference Between CP8D, Form E & EA Form?

Knowing the differences between these three forms is key to follow the rules .

|

Item |

CP8D |

Form E |

EA Form |

|

Nature |

Detailed employee data |

Employer annual declaration |

Employee income statement |

|

Submitted To |

LHDN |

LHDN |

Employee |

|

Prepared By |

Employer |

Employer |

Employer |

|

Submission Deadline |

31 March |

31 March |

Before 28 February |

|

Legal Basis |

Rule 8D |

Income Tax Act |

Income Tax Act |

CP8D and Form E are sent in together, while EA Form goes out to employees for their personal tax filing.

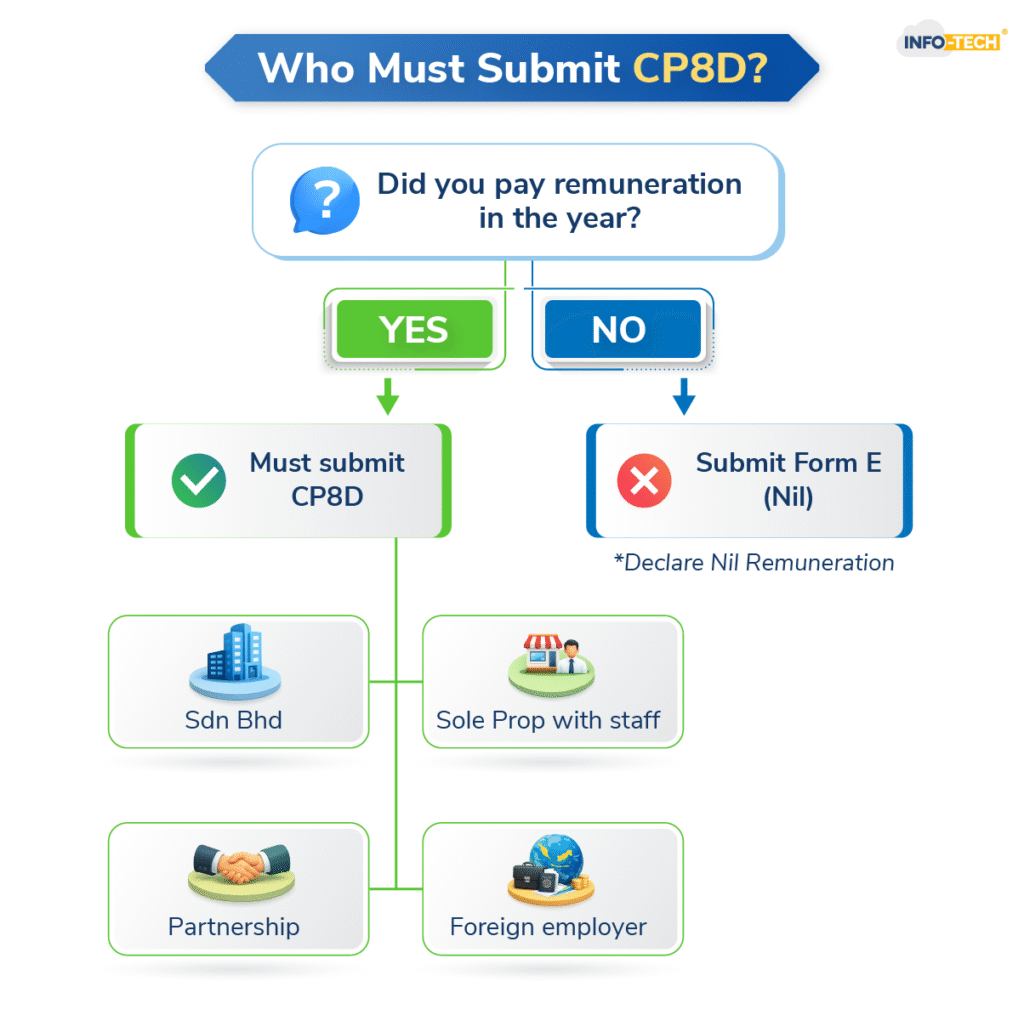

Who Needs to Send CP8D?

Each employer in Malaysia that has given remuneration to employees during the assessment year must submit CP8D.

This includes:

- Private limited companies (Sdn Bhd)

- Public companies (Berhad)

- SMEs and startups

- Sole proprietorships with staff

- Partnerships employing workers

- Representative offices

- Foreign entities employing Malaysian staff

- Companies with only one employee

Keep in mind, you need to send CP8D even if:

- The company didn’t take out PCB

- Staff worked for part of the year

- The business was not profitable

- An employee quit during the year

If the company paid remuneration, it needs to file CP8D.

What Happens If A Company Has No Staff?

When a business has no staff for the whole year, it still needs to send in Form E and say “Nil” for remuneration.

In these cases:

- You don’t need to send a CP8D employee file

- You still have to submit Form E through MyTax

- If you don’t send Form E, you might have to pay fines

LHDN wants yearly proof from registered employers even if there was no payroll activity.

What Information Should Be in CP8D?

CP8D includes complete salary details. Each employee’s record has:

- Full name

- NRIC / Passport number

- Income tax reference number (if they have one)

- Gross salary

- Bonus payments

- Allowances

- Benefits-in-kind

- Perquisites

- Director’s Fees

- PCB deducted during the year

- EPF Contributions

Getting this right matters a lot. LHDN’s system checks this info against what employees say on their tax forms.

How to Fill Out CP8D Form for 2026?

These days most employers send in CP8D online through LHDN’s MyTax website.

Step 1: Reconcile Your Year-End Payroll

Before you create CP8D, you need to reconcile:

- Your total yearly payroll reports

- Your monthly PCB filings (CP39)

- Your EPF payments

- EA Forms you gave your employees

This reconciliation makes sure your CP8D info matches your own payroll records.

Step 2: Make Your CP8D File

You can:

- Use LHDN’s e-Data Praisi program

- Create the needed text file with a compliant payroll software

- Format the file to fit LHDN’s prescribed structure

The layout must follow LHDN’s rules.

Step 3: Send It Through MyTax Portal

- Sign into MyTax (employer account)

- Fill out Form E

- Upload CP8D file

- Validate and confirm

- Download acknowledgment receipt

Companies should keep submission proof to show during audits and to meet compliance rules.

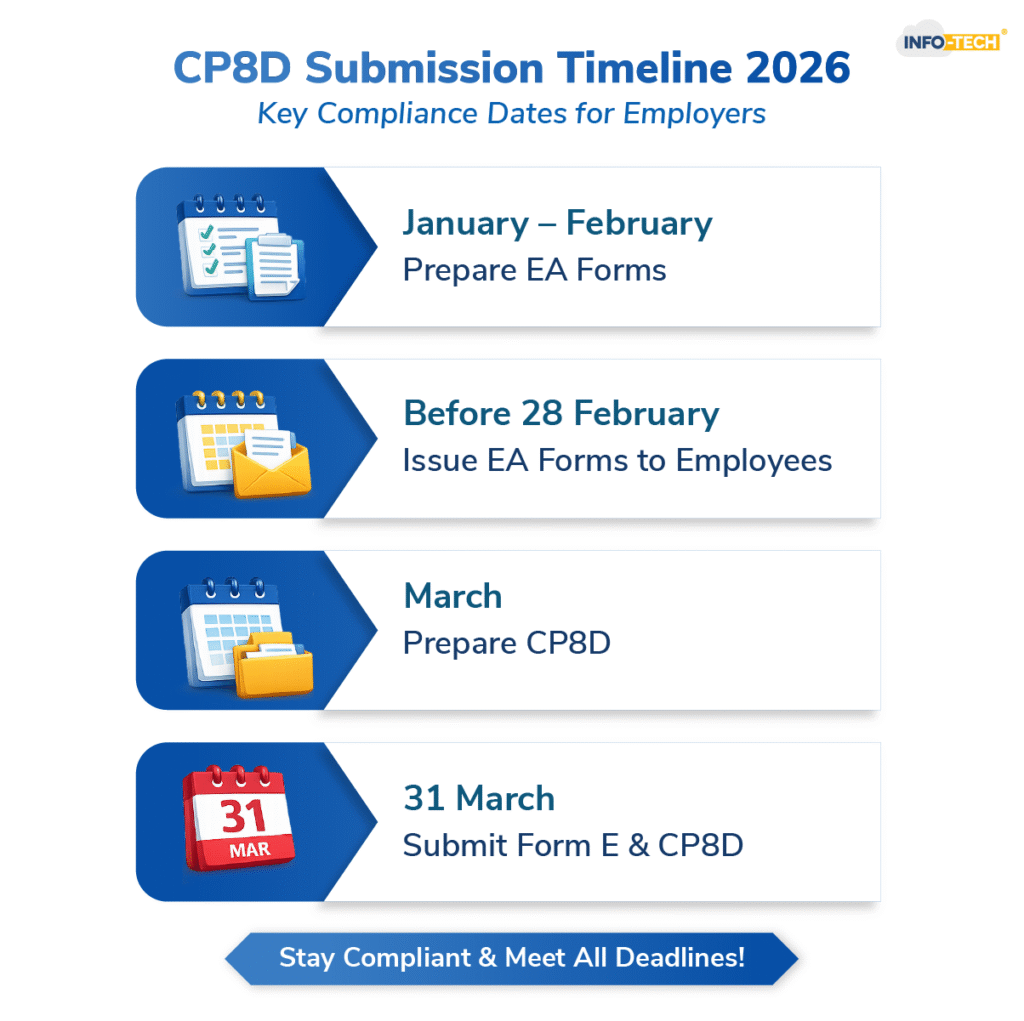

What is the Deadline For CP8D?

|

Submission |

Deadline |

|

EA Form to Employees |

Before 28 February |

|

Form E + CP8D to LHDN |

31 March (subject to official extensions) |

Turning in forms late might cause:

- Fines from RM200 to RM20,000

- Possible legal action

- Higher chance of an audit

- Compliance flags in LHDN’s system

It’s best to submit on time.

Conclusion

CP8D is a yearly submission that employers must make by law to ensure they report employee remuneration in Malaysia. It boosts tax transparency, helps verify PCB, and fits into Malaysia’s digital tax compliance setup.

For employers, CP8D isn’t just about filing taxes. It’s also:

- A way to check payroll

- A step to manage compliance risks

- A legal duty to report

- A responsibility in running the company well

Getting a good grasp of CP8D helps reduce errors, prevent penalties, and make sure yearly taxes goes through a smooth annual tax compliance.

CP8D FAQs

Who needs to submit CP8D?

All employers in Malaysia who paid remuneration to at least one employee during the year of assessment must submit CP8D together with Form E. This applies to companies, SMEs, sole proprietors, partnerships, and foreign employers with Malaysian employees, regardless of whether PCB was deducted.

What is Rule 8D of the Income Tax Rules?

Rule 8D of the Income Tax (Deduction from Remuneration) Rules 1994 requires employers to prepare and submit an annual return detailing remuneration paid to employees. It forms the legal basis for CP8D submission and ensures employer accountability in Malaysia’s self-assessment tax system.

How to fill CP8D if no employee LHDN?

If a company had no employees during the year, it must still submit Form E and declare “Nil” remuneration. A CP8D employee file is not required in this case, but failure to submit Form E may result in penalties.

How to fill CP8D form?

To fill CP8D, employers must compile annual payroll data including gross salary, allowances, bonuses, benefits-in-kind, PCB deductions, and EPF contributions. The data is formatted according to LHDN specifications and submitted electronically via MyTax together with Form E before the deadline.